Pre-Tax vs Roth: What Employees Should Know About Their 401(k) Options

Employees can direct their 401(k) contributions into pre-tax dollars, Roth dollars or a combination of the two. Understanding how each option works can help employees make more informed decisions about their savings.

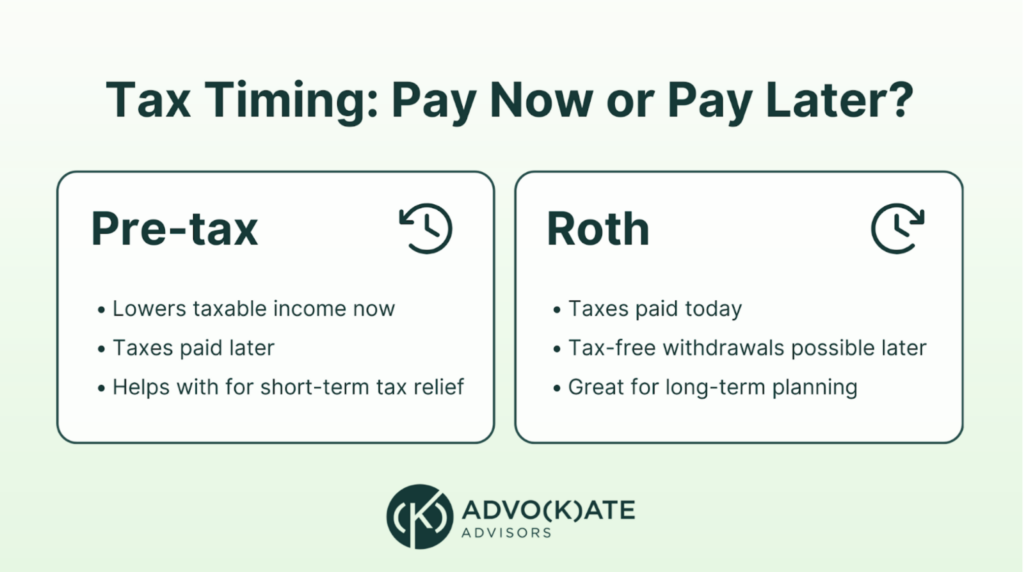

Pre-Tax Contributions

Pre-tax dollars go into the plan before taxes are taken out of the paycheck. This reduces taxable income for the year. The tradeoff is that withdrawals, your contributions plus all earnings, in retirement are taxed as regular income.

Roth Contributions

Roth dollars are contributed after taxes. If two requirements are met — reaching age 59½ and having made the first Roth contribution at least five years earlier — withdrawals can be taken tax-free. This allows savers to pay taxes now and avoid taxes on qualifying distributions later.

What Influences the Choice?

The choice often depends on current income, current tax bracket, projected income in retirement and expected tax bracket later in life. There is no single approach that works for everyone, so helping participants understand these differences can make it easier for them to select a contribution approach that supports their personal goals and long-term planning.